Build a Family Emergency Fund Fast: 2026 Guide

TL;DR:

- Building a family emergency fund quickly requires setting a clear target based on essential expenses and automating regular transfers. Using a separate high-yield savings account and tracking milestones helps maintain motivation and prevents impulsive spending during the saving process.

A family emergency fund is defined as a dedicated cash reserve covering 3–6 months of essential living expenses, held separately from everyday accounts. Building one fast is the single most effective step a family can take toward financial security. Financial experts recommend targeting this range because it covers job loss, medical bills, and major repairs without forcing families into debt. The good news: you do not need to save the full amount before you feel protected. Starting with a $1,000 starter fund builds real momentum and handles most minor emergencies right away.

How to build a family emergency fund fast: set your target first

The first step in any fast emergency fund strategy is knowing your exact number. Without a target, saving feels abstract and easy to postpone.

Essential expenses are the non-negotiable costs your family pays every month regardless of circumstances. They include:

- Housing: rent or mortgage payment

- Utilities: electricity, gas, water, and internet

- Groceries: food and household staples

- Insurance: health, auto, and renters or homeowners coverage

- Transportation: car payment, fuel, or public transit costs

- Minimum debt payments: credit cards, student loans, and personal loans

Exclude dining out, streaming subscriptions, gym memberships, and entertainment. Those are discretionary. They stop the moment a real emergency hits.

A practical calculation looks like this. Add up every essential expense above for one month. Multiply by three for your minimum target and by six for your full target. A family spending $3,500 per month on essentials needs $10,500 to $21,000 in total. That number can feel large, which is exactly why the staged approach works. Building the fund in stages — starter fund first, then one month, then three to six months — avoids overwhelm and increases success rates.

For a deeper breakdown of what counts as essential and how to calculate your personal target, the three to six months savings guide on the Amanahfund blog walks through the math clearly.

| Expense Category | Monthly Example | Include in Fund Target? |

|---|---|---|

| Rent or mortgage | $1,400 | Yes |

| Utilities | $250 | Yes |

| Groceries | $600 | Yes |

| Insurance | $350 | Yes |

| Transportation | $400 | Yes |

| Dining out | $200 | No |

| Streaming services | $50 | No |

| Entertainment | $150 | No |

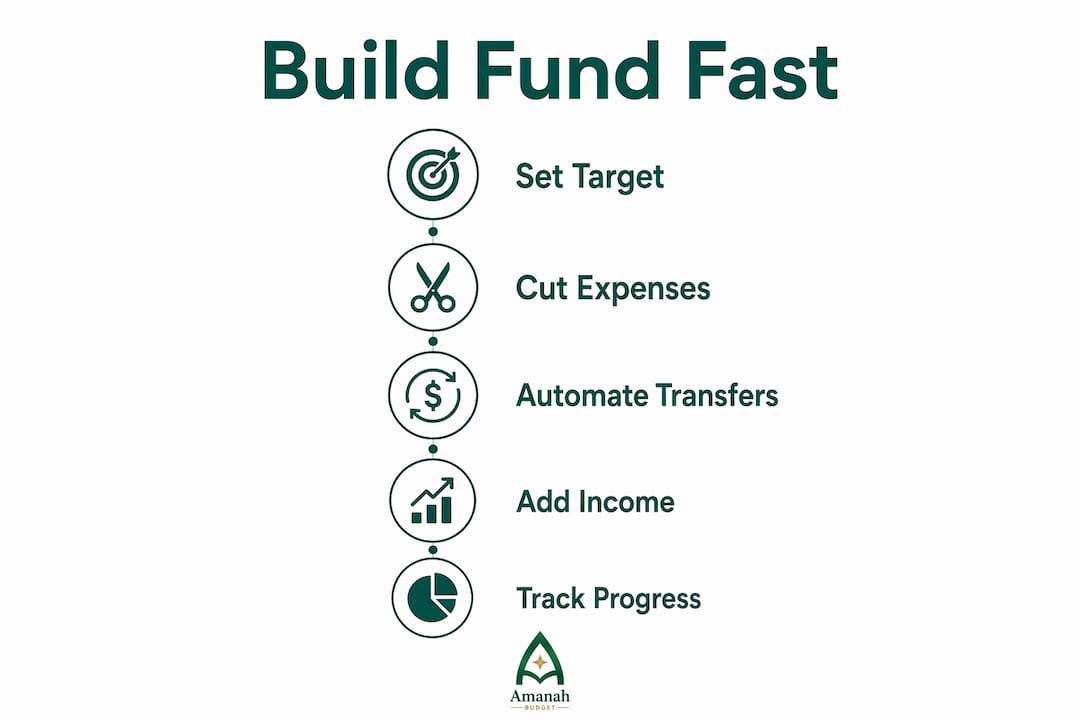

What are the fastest strategies to grow your emergency savings?

Speed comes from three levers: cutting expenses, automating transfers, and adding income. Use all three at once for the fastest results.

1. Run a survival budget for 90 days

A focused survival budget eliminates all non-essential spending temporarily to maximize saving capacity. This is not a permanent lifestyle change. Think of it as a 90-day sprint. Cancel subscriptions, pause eating out, and redirect every freed dollar to your emergency fund. Families who commit to this approach can redirect $100–$400 monthly just from auditing subscriptions, groceries, and bills in a 20-minute weekly review.

2. Automate transfers on payday

Set up an automatic transfer to a separate savings account the same day your paycheck arrives. Automating savings on payday removes the decision entirely. You never see the money in your checking account, so you never spend it. A $400 weekly automated transfer builds a $10,000 fund in roughly six months. Start smaller if needed. Even $50 per week adds up to $2,600 in a year.

3. Direct all windfalls to the fund

Tax refunds, work bonuses, cash gifts, and side income go directly into the emergency fund until you hit your target. This rule is simple and powerful. A single $1,500 tax refund can take you from a starter fund to one full month of expenses overnight.

4. Add a side income stream

Selling unused household items, picking up freelance work, or offering a skill on weekends accelerates the timeline significantly. Even one extra $200 per month shortens a six-month goal to under five months.

5. Set milestone targets

Starter funds of $500 to $1,000 handle most minor emergencies and build the psychological momentum to keep going. Celebrate each milestone. Reaching $1,000 is a genuine achievement worth acknowledging.

Pro Tip: Use meal planning to cut grocery costs. Meal planning reduces grocery spending by 25–40% for the average family of four. That savings alone can fund a $500 starter fund within two months.

What challenges stop families from saving fast, and how do you fix them?

Saving quickly is a behavioral challenge as much as a financial one. Knowing the obstacles in advance makes them easier to overcome.

Anxiety about the gap. Families who have no savings often feel paralyzed by how far they are from their goal. The fix is to shrink the target. Focus only on the next $500. Reaching that amount proves the system works and reduces anxiety immediately.

Dipping into the fund. The most common way families derail their progress is withdrawing from the emergency fund for non-emergencies. Keeping the fund at a separate institution with a 1–2 day transfer delay creates enough friction to prevent impulsive withdrawals. Out of sight genuinely means out of mind.

Losing motivation. Visual progress trackers work. A simple chart on the refrigerator showing your fund balance growing week by week reinforces saving habits and keeps the goal visible. Digital apps with goal-tracking features serve the same purpose.

Competing financial priorities. Families with debt often wonder whether to save or pay down balances. The answer: do both, but unequally. Make minimum payments on all debts and direct the rest toward the starter fund. Once you reach $1,000, reassess. Avoiding common budgeting mistakes during this phase keeps you from backsliding.

Treating your emergency fund as non-negotiable household infrastructure, as essential as your rent payment, is the mindset shift that separates families who build lasting financial resilience from those who stay stuck. Small, consistent contributions made every week matter far more than occasional large deposits.

Where should you keep your family emergency fund?

The right account protects your fund, earns interest, and stays accessible without being too easy to spend.

A high-yield savings account is the best choice for most families. High-yield savings accounts currently offer around 4–5% APY, compared to the near-zero rates on traditional savings accounts. On a $10,000 balance, that difference means $400–$500 in annual interest with zero risk. That is free money working for your safety net.

Avoid certificates of deposit (CDs) and investment accounts for emergency funds. CDs lock your money for a fixed term and charge penalties for early withdrawal. Investment accounts fluctuate in value. An emergency fund must be stable and liquid.

| Account Type | Accessibility | Interest Rate | Best For Emergency Fund? |

|---|---|---|---|

| High-yield savings account | 1–2 business days | 4–5% APY | Yes |

| Traditional savings account | Same day | 0.01–0.5% APY | Acceptable, not ideal |

| Certificate of deposit | Locked term | 4–5% APY | No |

| Investment account | 2–3 business days | Variable | No |

Keep the emergency fund at a different bank than your primary checking account. The slight inconvenience of a transfer delay is a feature, not a flaw. It stops you from treating the fund as a backup spending account.

Pro Tip: Set up round-up savings features if your bank offers them. Every debit card purchase rounds up to the nearest dollar, and the difference goes to savings. It is a painless way to add $20–$50 per month without changing any behavior. For families using halal-first tools, automating savings transfers through Amanahfund keeps the process values-aligned and consistent.

Before prioritizing high-yield accounts, make sure your emergency fund is fully funded before moving money into investments. As Oracle’s guide on investing mistakes points out, skipping the emergency fund to invest early is one of the most common and costly financial errors families make.

Key Takeaways

Building a family emergency fund fast requires a clear target, automated saving habits, and a separate account that protects the money from impulsive spending.

| Point | Details |

|---|---|

| Start with a starter fund | Reach $500–$1,000 first to build momentum and cover minor emergencies immediately. |

| Calculate essential expenses only | Base your target on housing, utilities, groceries, insurance, and transportation only. |

| Automate on payday | Schedule automatic transfers the day you get paid so the money never reaches your spending account. |

| Use a high-yield savings account | Earn 4–5% APY risk-free by storing your fund in a separate high-yield account. |

| Create transfer friction | Keep the fund at a different bank to prevent impulsive withdrawals without sacrificing accessibility. |

Why the mindset matters more than the math

I have worked with families at every income level, and the ones who build their emergency funds fastest share one thing: they stop treating savings as what is left over after spending. They treat it as a fixed expense, the same as rent.

The math is straightforward. The behavior is harder. Most families already know they should save three to six months of expenses. What stops them is not ignorance. It is the feeling that the goal is too far away to bother starting. That is why I always push the $500 starter fund first. It is reachable in weeks for most families, and reaching it changes something psychologically. The fund becomes real. The habit becomes real.

I have also seen families derail themselves by being too rigid. They aim for the full six-month target immediately, fall short one month, and give up entirely. Staged goals, as outlined in the family financial milestones guide, work because they give you wins along the way. Wins sustain effort.

One more thing families underestimate: talking about money together. When both partners know the goal, the timeline, and the current balance, the fund grows faster. Shared accountability is free and powerful.

— Imran

Amanahfund supports your family’s financial safety net

Muslim families deserve financial tools that reflect their values, and building a family safety net is one of the most important acts of care a household can take.

Amanahfund is a halal-first budgeting app built specifically for Muslim families. It includes dedicated emergency savings goals, AI-assisted transaction categorization, and shared household budgeting so both spouses stay aligned. Families can set up separate savings goals for emergencies, Hajj, Umrah, education, and more, all within a single values-aligned platform. No ads, no interest-based products, and no selling of user data. Visit Amanahfund to set up your family’s emergency fund goal today and start building financial resilience the halal way.

FAQ

How much should a family emergency fund cover?

Financial experts recommend 3–6 months of essential expenses, covering housing, utilities, groceries, insurance, and transportation only. Discretionary costs like dining out and subscriptions are excluded from the calculation.

What is the fastest way to start an emergency fund?

The fastest starting point is a $500–$1,000 starter fund, funded by automating a weekly transfer on payday and temporarily cutting all non-essential spending. Most families can reach this milestone within 4–8 weeks.

Should I save for an emergency fund or pay off debt first?

Make minimum payments on all debts and direct remaining funds toward a $1,000 starter fund first. Once the starter fund is in place, reassess the balance between debt repayment and continued emergency saving.

Where is the best place to keep an emergency fund?

A high-yield savings account at a separate bank is the best option. It earns 4–5% APY, stays liquid, and the 1–2 day transfer delay reduces the temptation to spend the money impulsively.

How do I stay motivated while building an emergency fund?

Use a visual progress tracker showing your current balance against your goal. Celebrate each milestone, starting with $500 and $1,000, to reinforce the habit and reduce anxiety about the larger target.

Recommended

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account