Islamic Pension Planning Explained for U.S. Muslims

TL;DR:

- Islamic pension planning involves creating a Shariah-compliant retirement strategy that excludes interest and forbidden industries. U.S. retirement accounts like IRAs and 401(k)s are permissible if their investments pass Shariah screening, and beneficiary designations must align with Quranic inheritance shares. If no halal options exist in an employer plan, contributing only up to the employer match and redirecting additional savings to personal halal accounts is permitted as a necessity.

Islamic pension planning is the process of building a halal, Shariah-compliant retirement strategy that grows your savings ethically while honoring Quranic financial stewardship responsibilities. The standard industry term for this practice is Shariah-compliant retirement planning, and both terms describe the same discipline. At its core, this approach requires avoiding riba (interest), excluding non-compliant industries, and distributing assets according to Faraid, the Quranic fixed inheritance system. Financial scholars widely recommend replacing 70–80% of pre-retirement income as a target, with a savings rate of roughly 15% of gross income annually.

What makes a retirement plan halal and Shariah-compliant?

A halal retirement plan excludes every investment that generates returns through interest or operates in a forbidden industry. That is a harder standard than most Muslims initially expect. Conventional 401(k) defaults often hold 30–50% in interest-bearing assets, so simply enrolling in your employer’s plan does not make your retirement savings halal.

Shariah screening removes four categories of investment:

- Interest-bearing instruments: conventional bonds, certificates of deposit, money market funds that pay interest

- Forbidden industries: alcohol, tobacco, gambling, adult entertainment, and conventional financial services that charge interest

- Excessive debt ratios: companies whose total debt exceeds roughly one-third of their market capitalization

- Impure revenue: companies that earn more than a small threshold of revenue from non-compliant activities

Compliant alternatives exist across every major asset class. Halal equities in Shariah-screened companies, sukuk (Islamic bonds structured around real asset ownership), and real estate investment trusts focused on permissible property types all qualify. Several halal ETFs are available for U.S. retirement accounts, giving Muslims access to diversified, screened portfolios without building individual stock lists from scratch.

Pro Tip: Ask any fund provider for its Shariah screening methodology and the name of its supervising Shariah board before investing. A fund without a named board and a published screening standard is not reliably compliant.

How can U.S. retirement accounts work for Islamic pension planning?

U.S. registered accounts like 401(k)s, Roth IRAs, and Traditional IRAs are Shariah-compliant as long as the underlying investments are halal-screened. The account structure itself carries no religious prohibition. The compliance question is always about what sits inside the account, not the account wrapper.

| Account Type | 2026 Contribution Limit | Key Tax Benefit | Halal Compatibility |

|---|---|---|---|

| Traditional IRA | $7,000 ($8,000 if 50+) | Tax-deferred growth | Yes, with screened funds |

| Roth IRA | $7,000 ($8,000 if 50+) | Tax-free withdrawals | Yes, with screened funds |

| 401(k) | $23,500 ($31,000 if 50+) | Employer match + deferral | Yes, if halal options exist |

The Roth IRA deserves special attention for Muslim investors. Contributions grow tax-free, and qualified withdrawals in retirement are also tax-free. That structure rewards long-term, patient investing, which aligns well with the Islamic principle of avoiding speculative short-term gains. A Roth IRA funded with halal ETFs or sukuk-based funds is one of the cleanest vehicles available for Sharia-compliant retirement building in the U.S.

The 401(k) presents more complexity. Employer plans often offer a limited fund menu, and many default options are target-date funds that hold significant bond allocations. Muslims who find no halal options in their employer’s menu face a real compliance challenge, addressed in detail below.

Pro Tip: Open a Roth IRA in your own name regardless of your employer plan situation. The $7,000 annual limit is modest, but decades of tax-free, halal-screened compounding creates meaningful retirement wealth.

What do Islamic inheritance laws mean for your pension?

Islamic inheritance law, known as Faraid, assigns fixed shares of an estate to primary heirs. U.S. probate courts do not automatically apply Faraid. Without a valid will that explicitly states Islamic inheritance allocations, state intestacy laws govern distribution, and those laws frequently conflict with Quranic shares.

The fixed shares under Faraid follow clear rules:

- Wife: receives 1/8 of the estate if children exist, or 1/4 if no children exist

- Husband: receives 1/4 of the estate if children exist, or 1/2 if no children exist

- Parents: each receives 1/6 if the deceased has children

- Discretionary bequests: capped at one-third of the total estate, directed to non-heirs or charitable causes

Retirement accounts like 401(k)s and IRAs pass outside of probate through beneficiary designations. That means your will alone does not control who receives these assets. You must update beneficiary forms on every retirement account to name heirs in proportions consistent with Faraid. Failing to do so can direct a large portion of your retirement wealth to a single named beneficiary, overriding the Quranic shares entirely.

Most probate disputes for Muslim estates arise from conflicts between secular wills and Faraid shares. A legally drafted will with explicit Faraid language, reviewed by both an Islamic scholar and a licensed U.S. attorney, reduces that risk significantly. Islamic estate planning basics require treating the will and the beneficiary designations as a coordinated system, not separate documents.

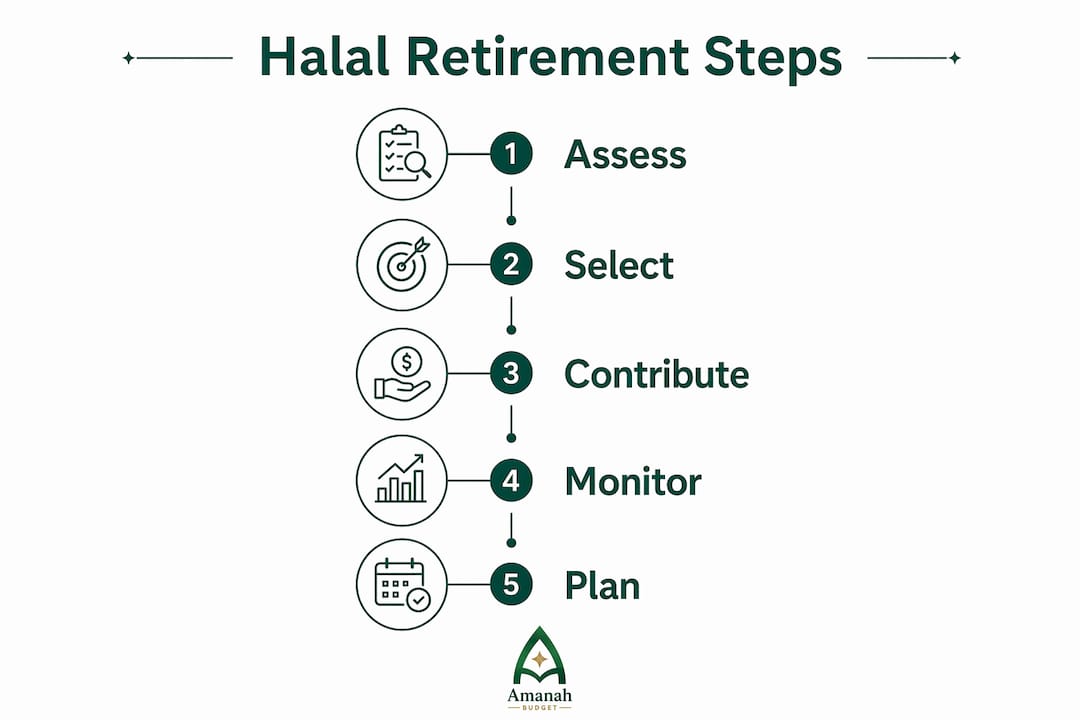

How to build a practical halal retirement portfolio

A sound halal retirement portfolio follows a clear sequence. Skipping steps creates gaps that force poor decisions later.

-

Build a halal emergency fund first. Keep 3–6 months of expenses in a non-interest account before directing money toward retirement. This prevents forced early withdrawals, which trigger taxes and penalties. Explore halal savings accounts that avoid interest entirely.

-

Eliminate high-interest debt. Carrying riba-based debt while investing creates a contradiction. Pay off credit card balances and conventional loans before maximizing retirement contributions.

-

Set a realistic income replacement target. The 70–80% income replacement benchmark is the standard planning goal. Calculate what that figure means in today’s dollars for your household, then work backward to determine how much you need to save monthly.

-

Save approximately 15% of gross income. Direct contributions across your 401(k), Roth IRA, and taxable halal accounts to reach this rate. Employer match contributions count toward the total.

-

Diversify across asset classes. A diversified halal portfolio spreads risk across Shariah-screened equities, sukuk, halal real estate, and cash equivalents. No single asset class should dominate.

-

Review compliance annually. Companies change their business activities. A fund that was Shariah-compliant three years ago may no longer qualify. Schedule an annual review of every holding against your chosen screening standard.

Pro Tip: Align your retirement savings horizon with your other Islamic financial goals. The same discipline that funds a Hajj savings plan builds the habit of consistent, purposeful saving for retirement.

What if your employer’s plan has no halal options?

This situation is more common than most Muslims realize. Many employers offer only a handful of funds, none of which pass Shariah screening. The scholarly response to this situation draws on the concept of rukhsa, a necessity-based exception.

Scholarly opinions differ on the details, but the general position is that participating in a non-compliant employer plan is permissible as a necessity when no halal alternative exists and forgoing participation means losing employer match contributions. The rukhsa applies narrowly. It covers capturing the employer match, not maximizing voluntary contributions beyond that threshold.

Practical steps when your employer plan lacks halal options:

- Contribute only up to the employer match. Capture the full match, then stop additional 401(k) contributions.

- Check for a self-directed brokerage window. Some 401(k) plans include a brokerage option that lets you purchase halal ETFs directly. Ask your HR department or plan administrator.

- Open a personal Roth IRA or Traditional IRA. Direct additional retirement savings into a self-managed account where you control fund selection entirely.

- Plan a rollover when you change jobs. When you leave an employer, roll the 401(k) balance into a self-directed IRA and immediately reinvest in halal-screened funds. This is the cleanest path to full compliance.

For retirement plan consulting on navigating employer plan structures and identifying compliant investment windows, working with a specialist familiar with both ERISA rules and Islamic finance principles produces the best outcomes.

Key Takeaways

Shariah-compliant retirement planning requires halal investment selection, coordinated beneficiary designations, and a legally enforceable Islamic will to protect both your savings and your heirs.

| Point | Details |

|---|---|

| Halal compliance is about investments, not accounts | 401(k)s and IRAs are permissible; the fund selections inside them determine compliance. |

| Faraid requires a coordinated will and beneficiary forms | Retirement accounts pass outside probate, so beneficiary designations must reflect Quranic shares. |

| Save 15% of gross income toward retirement | Target 70–80% income replacement and spread contributions across multiple account types. |

| Rukhsa permits limited non-compliant participation | Capture employer match in non-halal plans only; redirect excess savings to a personal halal IRA. |

| Annual compliance reviews protect your portfolio | Shariah screening status changes; review every holding once a year against a named screening standard. |

Why I think most Muslims underestimate the estate planning piece

The retirement savings conversation in Muslim communities has improved considerably over the past decade. More Muslims know about halal ETFs and Shariah-screened funds than ever before. What still gets overlooked, consistently, is the estate planning side.

Retirement accounts are often the largest single asset a family owns. A 401(k) worth $400,000 passes entirely to whoever is named on the beneficiary form, regardless of what your will says. I have seen families where a well-intentioned Muslim named only a spouse as beneficiary, not realizing that Faraid also allocates shares to children and parents. The will said one thing. The beneficiary form said another. The account went to the spouse alone.

The fix is not complicated, but it requires intentional coordination. Update beneficiary forms. Name multiple heirs in Faraid-consistent proportions. Have an Islamic scholar and a U.S. estate attorney review both documents together. The interfaith financial planning dimension matters here too, especially in households where spouses come from different backgrounds.

Scholars remind us that planning for our families is not a lack of trust in Allah. It is the fulfillment of our responsibility as stewards of what He has given us. Start early. Review annually. Do not leave your heirs to sort out what you could have clarified today.

— Imran

Amanahfund supports your halal financial planning

Amanahfund is built specifically for Muslim families who want their financial tools to reflect their values. The platform helps you track halal-aware spending, calculate zakat, and save intentionally for goals that matter, from Hajj to retirement.

Amanahfund’s halal-first approach means no interest-based products, no ads, and no selling of your data. Whether you are just starting to think about halal retirement investing or refining a plan you already have, Amanahfund gives you the structure and clarity to move forward with confidence. Built by Muslims, for Muslims.

FAQ

What is Islamic pension planning?

Islamic pension planning is the process of building a Shariah-compliant retirement strategy that avoids interest, excludes forbidden industries, and distributes assets according to Quranic inheritance rules.

Are 401(k)s and IRAs halal?

The account types themselves are permissible. Compliance depends entirely on the investments selected inside the account, specifically whether they pass Shariah screening.

What is Faraid and why does it affect my retirement plan?

Faraid is the Quranic system of fixed inheritance shares. Because retirement accounts pass through beneficiary designations rather than wills, you must name heirs in Faraid-consistent proportions on every account form.

What if my employer offers no halal 401(k) options?

Scholarly rulings permit contributing up to the employer match as a necessity exception. Direct additional retirement savings into a personal Roth IRA or Traditional IRA where you control fund selection.

How much should a Muslim save for retirement?

The standard benchmark is saving approximately 15% of gross income annually, targeting a retirement income of 70–80% of your pre-retirement earnings.

Recommended

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account