Why Financial Wellness Matters for Muslims: 2026 Guide

TL;DR:

- Financial wellness for Muslims involves managing money according to Islamic principles, including earning halal income and paying zakat. Building ethical wealth, practicing transparency, and balancing faith with financial planning deepen spiritual fulfillment and emotional health. Consistent habits like accurate zakat calculation and family financial conversations foster ethical stewardship and reduce financial stress.

Financial wellness for Muslims is defined as managing money according to Islamic principles to achieve personal stability, family security, and ethical fulfillment. This goes beyond basic budgeting. It means earning halal income, avoiding riba (interest), fulfilling zakat obligations, and building wealth in ways that honor both your dunya and your deen. Islamic financial literacy is a critical driver of financial well-being among Muslims, with higher literacy consistently linked to stronger financial management. For Muslim families, financial health is not a secular goal. It is an act of worship and stewardship rooted in amanah, the trust Allah places in us over the resources we hold.

Why financial wellness matters for Muslims: the Islamic foundation

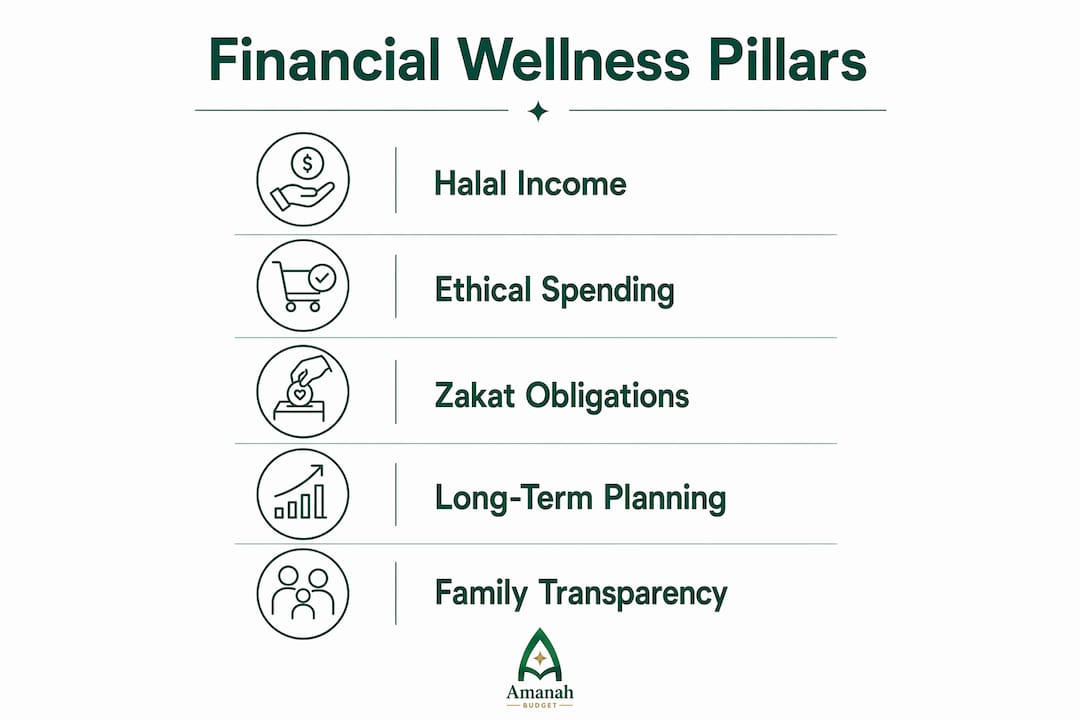

Financial wellness in an Islamic context rests on four pillars: halal income, ethical spending, obligatory giving, and long-term planning. Each one connects directly to Shariah principles that have guided Muslim communities for centuries.

Halal income is the starting point. Earnings from prohibited sources, including riba, gambling, and haram industries, corrupt the entire financial picture. Shariah requires that wealth enters the household through permissible means before any other financial practice can be considered sound.

Zakat is the most misunderstood pillar. It is not optional charity. Zakat is mandatory for any Muslim whose net wealth exceeds the nisab threshold, approximately the value of 85 grams of gold, held for a full lunar year. That threshold matters because many families underestimate their zakatable assets by excluding savings, gold jewelry, or investment accounts. Paying zakat correctly purifies wealth and fulfills a direct obligation to the community.

Balanced spending follows the Quranic principle of avoiding both israf (waste) and taqtir (miserliness). Islam does not ask Muslims to live in austerity. It asks for intentional, proportionate spending that reflects gratitude and responsibility.

Long-term planning includes building an emergency fund, establishing a wasiyyah (Islamic will), and making Shariah-compliant investments. A Muslim family financial goals plan that incorporates all four pillars creates a structure that is both spiritually grounded and practically sound.

| Component | Description |

|---|---|

| Halal income | Earnings from permissible sources, free from riba and haram industries |

| Zakat | Mandatory annual giving on net wealth above the nisab threshold |

| Balanced spending | Avoiding waste and miserliness; spending with intention and gratitude |

| Emergency fund | Savings buffer that prevents debt in times of hardship |

| Wasiyyah | Islamic will that distributes wealth according to Shariah after death |

Pro Tip: Calculate your zakat on net zakatable wealth, not just cash on hand. Include savings accounts, gold, silver, and investment portfolios. Many families underpay because they exclude these categories.

How does financial wellness affect Muslim mental and emotional health?

Financial stress is one of the most damaging forces in family life. Financial stress affects one-third of working adults, with measurable impact on mental and physical health. That statistic applies across all communities, but Muslim families face a unique layer of complexity when their financial reality conflicts with their values.

The concept of tawakkul, trusting in Allah’s provision, is sometimes misapplied in ways that increase anxiety rather than reduce it. This is what researchers and Islamic finance educators call weaponized tawakkul: using reliance on God as a reason to avoid planning, budgeting, or addressing debt. True tawakkul supports calm, proactive stewardship. It does not replace it.

“True financial stability in Islam combines practical effort, trust in Allah, and ethical conduct. This integration transforms financial planning from a source of stress into an act of worship and peace.” Psychology Healthcare 2026

Family financial transparency also plays a direct role in emotional well-being. When spouses and household members share financial information openly, conflicts over money decrease. Families that practice financial consultation, known as Shura, report greater alignment on spending priorities, giving goals, and savings targets. The result is not just better numbers. It is a calmer, more unified household.

Common emotional challenges Muslim families face include:

- Shame around debt, which prevents seeking help or making a plan

- Anxiety from not knowing whether their spending is halal-compliant

- Conflict between spouses when financial decisions are made unilaterally

- Guilt from missing zakat obligations due to confusion about calculation

Each of these challenges has a practical solution rooted in Islamic financial education and consistent practice.

What practical steps can Muslims take to improve financial health?

Improving financial health as a Muslim does not require a complete overhaul. It requires consistent, faith-aligned habits built one at a time. Financial wellness is built on small, consistent efforts like maintaining an emergency fund and clear budgeting, and these steps build confidence over time.

-

Track halal income and categorize spending. Start by mapping every income source and confirming it is permissible. Then categorize your spending to identify where money goes each month. Tools that support halal-aware budgeting make this process faster and more accurate.

-

Calculate and schedule zakat correctly. Zakat applies on net wealth including savings, gold, and investments above the nisab threshold. Set a fixed date each lunar year to calculate and pay. Treat it as a line item in your budget, not an afterthought.

-

Build an emergency fund before investing. Three to six months of living expenses in a halal savings account creates a buffer that prevents reliance on interest-bearing debt during hardship. This fund is not a luxury. It is a financial obligation to your household.

-

Incorporate sadaqah into your monthly plan. Voluntary giving beyond zakat strengthens the habit of generosity and keeps wealth in circulation within the community. Budget a fixed amount each month, even if it is small.

-

Build Shariah-compliant investment habits. Halal investing excludes interest-bearing instruments, companies in prohibited industries, and excessive speculation. Shariah-compliant equity funds and sukuk (Islamic bonds) offer accessible entry points for Muslim families building long-term wealth.

-

Hold a monthly family financial council. A monthly Shura meeting creates shared accountability. Review the budget together, confirm zakat calculations, discuss upcoming goals like Hajj or education savings, and make decisions jointly.

Pro Tip: Use a halal-first budgeting app that separates zakatable assets from general spending automatically. Manual tracking works, but purpose-built tools reduce errors and save time every month.

Reviewing your monthly budget Islamically is a practice that connects your financial decisions to your values in real time. It turns a routine task into a meaningful act of stewardship.

What misconceptions hold Muslims back from financial wellness?

Several widely held beliefs prevent Muslim families from achieving the financial health they deserve. Identifying them clearly is the first step toward correcting them.

Misconception 1: Tawakkul means not planning. This is the most damaging belief in Muslim financial culture. Correct tawakkul balances reliance on Allah with proactive planning. The Prophet Muhammad (peace be upon him) instructed believers to tie their camel before trusting in Allah. Planning is not a lack of faith. It is an expression of it.

Misconception 2: Avoiding haram is enough. Focusing solely on avoiding haram misses the positive pillars of Islamic finance. Zakat, sadaqah, and halal investing are not optional extras. They are core obligations and opportunities that build household stability.

Misconception 3: Zakat is simple to estimate. Most families miscalculate zakat by using informal valuations. Proper zakat calculation requires measuring all net zakatable wealth, including savings, gold, and investments, against the nisab threshold at the correct lunar date.

Misconception 4: Talking about money is taboo. Financial silence in families creates hidden debt, missed zakat, and unresolved conflicts. Open financial communication, guided by Shura principles, is both permitted and encouraged in Islam.

Pitfalls to avoid and their corrections:

- Pitfall: Estimating zakat informally. Correction: Use a structured zakat calculator that accounts for all asset categories.

- Pitfall: Skipping the emergency fund to invest faster. Correction: Build three months of expenses in savings before any investment.

- Pitfall: Making financial decisions without a spouse’s input. Correction: Hold a monthly family financial council to align on goals.

- Pitfall: Treating sadaqah as optional when money is tight. Correction: Budget a fixed, small amount monthly so giving remains consistent.

- Pitfall: Using conventional financial tools that mix halal and haram categories. Correction: Choose tools designed with Islamic values built in from the start.

Understanding financial security fundamentals alongside Islamic principles gives Muslim families a complete picture of how to protect and grow their wealth ethically.

Key Takeaways

Financial wellness for Muslims requires combining halal income, correct zakat, balanced spending, and family transparency into one consistent practice.

| Point | Details |

|---|---|

| Halal income is the foundation | All financial wellness begins with permissible earnings free from riba and haram sources. |

| Zakat requires precise calculation | Measure all net zakatable assets annually against the nisab threshold, not just cash savings. |

| Tawakkul supports planning | True reliance on Allah includes proactive budgeting and financial preparation, not avoidance. |

| Family Shura reduces conflict | Monthly financial councils align spouses on goals, spending, and giving obligations. |

| Consistent small steps build wellness | Emergency funds, monthly budgeting, and regular sadaqah create lasting financial stability. |

Why faith and finance belong together

I have spent years watching Muslim families treat financial planning as a secular concern, something separate from their deen. That separation is the root of most financial anxiety I observe in our community. When you disconnect money from your values, every financial decision becomes harder because it lacks a moral anchor.

What I have found is that the families who thrive financially are not the ones with the highest incomes. They are the ones who hold a monthly Shura meeting, who calculate zakat with care rather than guessing, and who treat their emergency fund as a form of gratitude for what they have been given. These are not complicated practices. They are consistent ones.

The concept of amanah, trusteeship, reframes the entire conversation. You are not the owner of your wealth. You are its steward. That shift in perspective removes the ego from financial decisions and replaces it with responsibility. It also removes the shame. You are not managing money for status. You are managing it for a purpose.

My honest observation is that Islamic financial wellness is not harder than conventional financial wellness. It is actually clearer. The rules are defined. The obligations are known. The goals are meaningful. What most families need is not more information. They need a structure that makes those values visible in their daily financial life.

— Imran

Amanahfund: built for Muslim financial wellness

Amanahfund’s halal budgeting app gives Muslim families a purpose-built structure for every principle covered in this article.

Amanahfund tracks spending with halal-aware categories, calculates zakat using your preferred madhab, and supports savings goals for Hajj, Umrah, Ramadan, Eid, and education. Spouses can share a household budget in real time. AI-assisted transaction categorization reduces the manual work of sorting halal from non-compliant spending. There are no ads, no data sales, and no interest-based products. Explore the Islamic wealth tracking guide on the Amanahfund blog to see how these tools work in practice, then set up your family’s first halal budget with confidence.

FAQ

What is financial wellness in Islam?

Financial wellness in Islam means managing money according to Shariah principles, including earning halal income, paying zakat, avoiding riba, and spending with intention. It connects practical financial health to spiritual responsibility.

Why is zakat important for financial wellness?

Zakat purifies wealth and fulfills a mandatory obligation on net assets above the nisab threshold held for a full lunar year. Correct, timely zakat payment is a core component of Islamic financial health, not an optional act of charity.

What is weaponized tawakkul?

Weaponized tawakkul is the misuse of trust in Allah as a reason to avoid financial planning. True tawakkul combines reliance on Allah with proactive, responsible stewardship of money and resources.

How does a family financial council improve financial wellness?

A monthly family financial council, based on the Islamic principle of Shura, creates shared accountability for budgets, zakat, and savings goals. Regular meetings reduce financial conflict and align household members on priorities.

Why is Islamic financial literacy important?

Higher Islamic financial literacy is consistently associated with improved financial management and stronger financial well-being. Families who understand both Islamic obligations and practical financial tools make better, more confident decisions.

Recommended

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account