Muslim Family Retirement Planning Explained: 2026 Guide

TL;DR:

- Muslim families should prioritize halal retirement planning based on Islamic principles and ethical investing. They must choose compliant accounts, avoid interest, pay zakat, and regularly review their investments to ensure ongoing compliance. Consistent saving, clear family goals, and annual purification are essential to building a financially and spiritually sound retirement.

Muslim family retirement planning is the process of securing a financially stable, Shariah-compliant retirement by integrating Islamic obligations, ethical investing principles, and consistent savings habits. The standard industry term for this practice is halal retirement planning, and it covers everything from avoiding riba to selecting the right tax-advantaged accounts. For Muslim families, this is not just a financial exercise. It is an act of amanah, a sacred trust to protect and provide for those who depend on you. This guide covers the core Islamic principles, the best savings vehicles, practical savings benchmarks, and the ongoing steps that keep your retirement funds both sufficient and spiritually sound.

What are the core Islamic financial principles guiding retirement planning?

Halal retirement planning rests on four non-negotiable principles. Each one shapes which accounts you open, which funds you select, and how you manage wealth over time.

- Avoidance of riba (interest). Standard bond funds and savings accounts that earn fixed interest are not permissible. Retirement portfolios must replace these with Shariah-compliant alternatives such as sukuk, which are asset-backed instruments that generate returns through profit-sharing rather than interest payments.

- Zakat on accumulated wealth. Zakat is obligatory annually on net wealth exceeding the nisab threshold, approximately the value of 85 grams of gold, held for one full lunar year. This applies to retirement account balances, not just cash on hand. Paying zakat correctly preserves the spiritual integrity of your entire retirement plan.

- Debt management before investing. High-interest consumer debt contradicts Islamic principles. Families should eliminate interest-bearing liabilities before directing significant funds into long-term retirement accounts.

- Ethical investing through Shariah screens. Funds must exclude companies involved in alcohol, tobacco, conventional banking, weapons manufacturing, and other prohibited industries. Most halal fund providers apply AAOIFI (Accounting and Auditing Organization for Islamic Financial Institutions) screening standards.

- Risk-sharing and asset backing. Permissible investments must be tied to real economic activity. Sukuk, real estate investment trusts screened for halal compliance, and equity in permissible businesses all satisfy this requirement.

Pro Tip: Before selecting any mutual fund or ETF for your retirement account, request the fund’s Shariah compliance certificate or check whether it follows AAOIFI or MSCI Islamic Index screening criteria. A fund labeled “socially responsible” is not automatically halal.

Which retirement accounts and savings vehicles are halal for Muslims?

The account type itself is not what makes a retirement vehicle halal or haram. The underlying investments inside the account determine compliance.

Tax-advantaged accounts in the U.S.

A 401(k), Roth IRA, or traditional IRA is fully permissible when the funds held inside avoid interest-bearing bonds and prohibited industries. 2026 IRS contribution limits set the IRA ceiling at $7,500 per year ($9,500 for those aged 50 and older) and the 401(k) ceiling at $24,000 ($31,500 for those aged 50 and older). These limits represent a meaningful annual opportunity to build tax-sheltered halal wealth.

The Roth IRA is particularly attractive for Muslim families in lower tax brackets today, since qualified withdrawals in retirement are completely tax-free. The key step is selecting a brokerage that offers Shariah-screened funds within the account, or self-directing into halal ETFs and sukuk.

Canadian options

Canadian Muslim families can use the Registered Retirement Savings Plan (RRSP) and the spousal RRSP. Spousal RRSPs allow income splitting when withdrawals are delayed at least three calendar years after the last contribution, which improves tax efficiency and builds financial independence for the lower-earning spouse. This structure is especially useful in single-income Muslim households.

Emergency fund first

A 3–6 month emergency fund held in a non-interest-bearing halal savings vehicle must come before any long-term investing. Without this buffer, a job loss or medical expense can force early withdrawals from retirement accounts, triggering penalties and tax losses that set back years of growth.

| Account type | Permissible? | 2026 contribution limit | Key condition |

|---|---|---|---|

| Roth IRA | Yes | $7,500 ($9,500 if 50+) | Invest only in halal funds |

| Traditional IRA | Yes | $7,500 ($9,500 if 50+) | Avoid interest-bearing bonds |

| 401(k) | Yes | $24,000 ($31,500 if 50+) | Select Shariah-screened options |

| Spousal RRSP (Canada) | Yes | Per RRSP room | Delay withdrawals 3+ years |

Pro Tip: If your employer’s 401(k) plan does not offer a Shariah-compliant fund option, contribute only enough to capture the full employer match, then direct additional savings into a self-directed Roth IRA where you control the fund selection.

How much should Muslim families save and invest for retirement?

The standard benchmark for retirement savings is 15% of gross annual income, directed consistently into halal investments over a working career. Saving 15% of gross income over 30–35 years in halal investments, assuming an average annual portfolio return of 7%, can accumulate approximately $2.3 million by retirement age. That figure assumes $33,000 in annual savings from a $220,000 household income. The math confirms that consistency matters far more than timing the market.

Families who start later or carry heavier obligations, such as supporting parents or funding children’s education, may need to raise their savings rate to 18%–20% to compensate. Conversely, families with defined pension income or significant real estate equity can sometimes sustain a lower contribution rate.

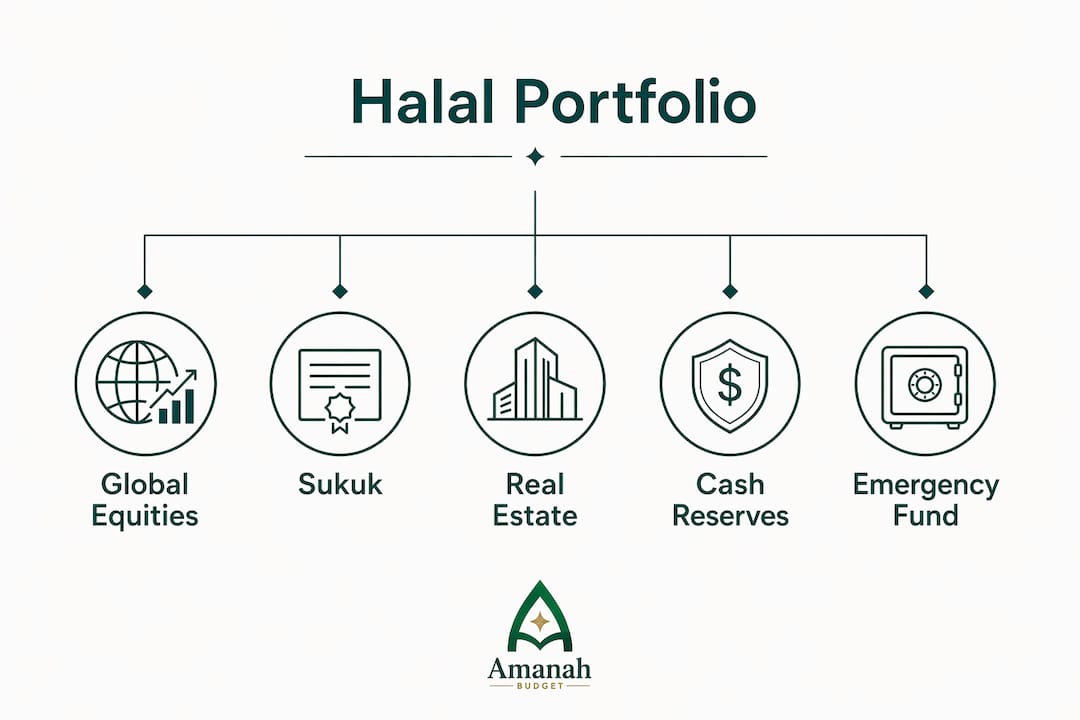

Diversification within a halal portfolio

A well-structured halal retirement portfolio typically combines three asset classes. Shariah-screened global equities provide long-term growth. Sukuk funds, which you can compare alongside thematic fixed income options to understand how asset-backed instruments differ from conventional bonds, provide stability. Halal real estate exposure, through screened REITs or direct property ownership, adds inflation protection.

| Years to retirement | Suggested equity allocation | Suggested sukuk allocation | Notes |

|---|---|---|---|

| 30+ years | 80%–90% | 10%–20% | Maximize growth phase |

| 15–29 years | 60%–75% | 25%–40% | Begin gradual shift |

| Under 15 years | 40%–55% | 45%–60% | Prioritize capital preservation |

Delay in saving or defaulting to non-compliant plans is the single greatest risk to retirement security among Muslim professionals, not income level. Starting five years later can reduce a final portfolio by hundreds of thousands of dollars due to lost compounding.

What ongoing actions maintain the halal status of retirement funds?

Setting up a halal portfolio is the beginning, not the finish line. Three recurring actions keep retirement funds both compliant and growing.

- Annual purification of investment gains. Even Shariah-screened funds may hold a small percentage of non-compliant revenue, often less than 5%. Purification requires calculating that non-compliant income portion from the fund’s prospectus and donating that exact amount to charity each year. This is separate from zakat and is not optional for families committed to full halal compliance.

- Annual zakat payment on retirement balances. Retirement account balances that meet the nisab threshold and have been held for one lunar year are zakatable. Calculate zakat at 2.5% of the net zakatable amount. Families should track this alongside other zakatable assets such as cash, gold, and business inventory.

- Shariah screen reviews. Fund holdings change. A fund that passed screening last year may hold a newly non-compliant company today. Review your fund’s Shariah compliance report at least once per year, or use a fund provider that publishes quarterly screening updates.

- Portfolio rebalancing as retirement nears. Shift gradually from growth equities toward sukuk funds in the decade before retirement. Shariah lifestyle strategies increasingly automate this risk adjustment, simplifying compliance within workplace pension structures.

- Avoid premature withdrawals. Early withdrawals from 401(k) or IRA accounts before age 59½ trigger a 10% federal penalty plus income tax. Beyond the financial cost, forced early withdrawals often result from inadequate emergency savings, which is why the halal liquidity buffer matters so much.

Pro Tip: Keep a simple annual checklist: pay zakat, calculate purification amount, review fund screening reports, and rebalance allocations. Treat this like a yearly financial audit tied to Ramadan or the start of the Islamic new year.

How should Muslim families coordinate retirement planning with broader family goals?

Retirement does not exist in isolation from the rest of a Muslim family’s financial life. Shared financial visibility between spouses and joint goal setting increase financial harmony and improve retirement planning outcomes. Explicit alignment on goals such as Hajj funding, children’s education, and retirement adequacy prevents future conflict and keeps both spouses accountable.

A practical approach to family financial goal setting places goals into three tiers:

- Immediate obligations: zakat, debt repayment, emergency fund

- Medium-term goals: Hajj savings, children’s education, home purchase

- Long-term goals: retirement accounts, estate planning, sadaqah endowments

Islamic inheritance law (faraid) requires that estate distribution follow Quranic guidelines. This means retirement beneficiary designations and estate documents must be reviewed by someone familiar with faraid, not just a standard estate attorney. A will that conflicts with faraid creates legal and spiritual complications for heirs.

Transparency between spouses on all financial accounts, including retirement balances, is not just good practice. It is a foundation of trust that the best budgeting strategies for Muslim families consistently identify as a key driver of long-term financial success. Families that plan together, review together, and give together build retirement security that reflects their values at every level.

Key Takeaways

Halal retirement planning requires consistent savings, Shariah-compliant investment selection, annual zakat and purification, and coordinated family goal setting to build sufficient and spiritually sound retirement wealth.

| Point | Details |

|---|---|

| Start with Islamic principles | Avoid riba, pay zakat annually, and screen all investments against AAOIFI standards. |

| Use tax-advantaged accounts | 401(k), Roth IRA, and RRSP are all permissible when funded with halal investments. |

| Save 15% of gross income | Consistent 15% savings in halal funds can build approximately $2.3 million over 30–35 years. |

| Purify and review annually | Calculate non-compliant income portions and donate them to charity, separate from zakat. |

| Coordinate as a family | Align retirement goals with Hajj, education, and estate planning for unified household progress. |

Why I think most Muslim families are solving the wrong retirement problem

The families I see struggle most with retirement planning are not the ones with low incomes. They are the ones with high incomes and deep uncertainty about whether halal options are “good enough” to build real wealth. That uncertainty leads to delay. And delay, compounded over a decade, is far more damaging than any suboptimal fund selection.

The uncomfortable truth is that the halal investing universe has expanded dramatically. Shariah-screened equity funds have historically tracked closely to conventional benchmarks over long periods. The compliance gap that existed 20 years ago is largely closed. Families who wait for a “perfect” halal solution often miss years of compounding that no future correction can recover.

My honest advice is this: start with what is available, purify what needs purifying, and refine as you learn. A Roth IRA funded with a Shariah-screened global equity ETF, opened this month, beats a theoretically perfect portfolio that never gets funded. Faith-guided financial planning is not about perfection. It is about consistent, intentional action aligned with your values. That combination, over time, is what actually builds security for your family.

— Imran

Amanahfund: halal-first financial tools for Muslim families

Retirement planning works best when your day-to-day finances are already organized around Islamic values. Amanahfund is a halal-first budgeting app built specifically for Muslim families, with features that make it easier to track spending, calculate zakat, and save intentionally for goals like Hajj, education, and retirement.

Amanahfund includes halal-aware spending categories, AI-assisted transaction categorization, and shared household budgeting so both spouses stay aligned. Zakat calculation follows your preferred madhab. Savings goals for Hajj, Umrah, Ramadan, and emergencies are built directly into the experience. No ads, no data selling, and no interest-based products. Visit Amanahfund to see how a budgeting tool built around your deen can support your long-term retirement goals.

FAQ

What makes a retirement account halal for Muslims?

A retirement account is halal when the investments held inside it avoid interest-bearing instruments and prohibited industries. The account structure itself, whether a 401(k), Roth IRA, or RRSP, is permissible as long as you select Shariah-compliant funds within it.

How much zakat do I owe on my retirement savings?

Zakat is due at 2.5% of retirement account balances that exceed the nisab threshold and have been held for one full lunar year. This applies to the full zakatable balance, not just annual contributions.

What is income purification in halal investing?

Purification is the process of calculating the percentage of non-compliant revenue within a Shariah-screened fund and donating that exact amount to charity each year. It is separate from zakat and is required to maintain full halal compliance in your portfolio.

Is a Roth IRA better than a traditional IRA for Muslim families?

A Roth IRA is generally better for Muslim families in lower or mid-range tax brackets today, since qualified withdrawals in retirement are completely tax-free. The right choice depends on your current versus expected future tax rate.

How do I coordinate retirement planning with Hajj and education savings?

Organize goals into tiers: fulfill immediate obligations like zakat and emergency savings first, then fund medium-term goals like Hajj and education, then direct remaining capacity into retirement accounts. Shared goal-setting between spouses, reviewed regularly, keeps the household aligned across all three tiers.

Recommended

Ready to manage your amanah?

Track halal spending, calculate zakat, save for Hajj — all in one app. Free forever.

Create Free Account